I was having coffee with a friend in Colombo last week, and he was wrestling with where to park some savings. “Should I buy a small plot of land down south,” he asked, “or just put it into a few good stocks on the CSE?” It’s a classic Sri Lankan dilemma, and honestly, the old answers don’t always hold up anymore.

For generations, the default has been property. It feels safe, right? You can see it and touch it. But then you see the All Share Price Index (ASPI) make a significant move, and you can’t help but wonder if you’re missing out on a different kind of growth. We’re talking about two completely different approaches to building wealth; one is often a slow, steady marathon, while the other can be a sprint with some serious hurdles.

So, which path is actually right for you? I think it depends entirely on your capital, your timeline, and your stomach for risk. In this breakdown, we’re going to look past the hype. We’ll compare the hidden costs of property ownership against the market volatility of stocks, giving you a clear framework to decide which strategy truly fits your personal financial goals.

Understanding the Post-Crisis Investment Climate in Sri Lanka

Let’s be honest, thinking about investing after what we went through in 2022 feels like a massive shift. For a long time, it was about financial survival, not growth. But things are genuinely starting to look different, and I think it’s the right time to start cautiously planning for the future again. The economic environment today is a world away from the chaos of just two years ago, but you need to understand the new rules of the game.

The Macro-Economic Picture: What’s Changed?

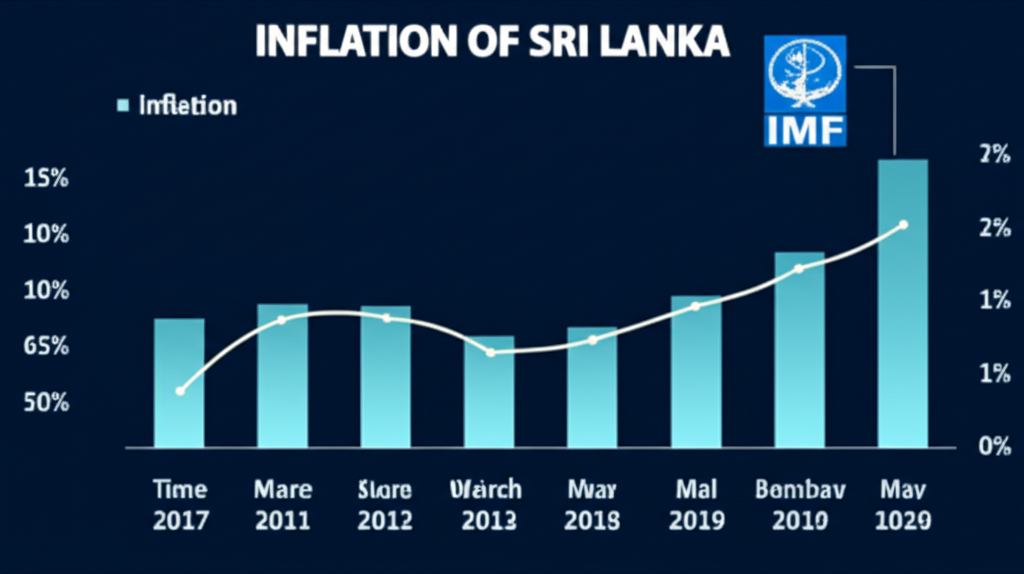

The biggest change, without a doubt, has been the taming of inflation. Remember when prices were doubling overnight? That’s over. Inflation plummeted from a staggering 70% to just 0.9% by May 2024. This is huge because it means your money isn’t losing its value while it sits in the bank. At the same time, the Central Bank has been cutting policy rates, bringing them down to 8.5% by June 2024. This makes borrowing for something like a property cheaper, but it also means fixed deposits won’t give you the returns they used to. The Sri Lankan Rupee has also shown remarkable strength against the US Dollar, which signals a return to some form of stability.

The IMF Factor and Investor Confidence

The IMF program has been a tough pill to swallow, but it has provided a much-needed dose of discipline. Think of it as a strict financial recovery plan that forces the government to stick to targets. This external validation, combined with progress on debt restructuring, has slowly rebuilt confidence both locally and internationally. It’s why organizations like the World Bank are forecasting a modest but positive GDP growth of 2.2% for 2024. So, is everything perfect? Of course not. But for the first time in a while, there’s a predictable path forward, which is exactly what investors need.

Investing in Bricks and Mortar: The Sri Lankan Real Estate Market

Let’s shift gears for a moment. There’s a certain comfort in property, isn’t there? You can see it, touch it, and for many Sri Lankans, it feels like the most secure investment you can make. I think it’s this tangibility that draws us in. Beyond just owning a physical asset, property can be a workhorse. You get the potential for steady rental income, which, according to LankaPropertyWeb, can yield around 4-6% in Colombo. Plus, it’s a classic hedge against inflation. As the cost of living rises, so do property values and rents, protecting your purchasing power over the long run.

But it’s not all smooth sailing. The biggest hurdle is obviously the high capital needed to even get started. Unlike stocks, you can’t just buy a small piece of a house. Property is also notoriously illiquid. Selling a piece of land or an apartment can take months, sometimes longer, so your money is tied up. Then you have the paperwork and taxes. You’ll need a good lawyer to navigate title deeds, and you must factor in costs like the 1% Stamp Duty and potential Capital Gains Tax (CGT) if you sell for a profit. These aren’t small details; they directly impact your returns.

Popular Strategies and Locations

So, where are people putting their money? Colombo and its suburbs are perennial favourites, especially for apartments. We saw condominium prices in Colombo increase by 8.5% in 2022 alone, based on a CBRE Sri Lanka report. Galle and Kandy also attract significant investment, blending lifestyle appeal with tourism potential. For those with a higher risk appetite, I’ve seen a lot of interest in emerging coastal areas from Kalpitiya down to Arugam Bay.

As for how to invest, there are a few common paths:

Buy-to-Let: This is the most popular strategy. For example, buying a two-bedroom apartment in a place like Rajagiriya for around LKR 35 million, then renting it out to a young professional couple or a small family. Your goal is to have the rent cover your mortgage and maintenance, with a little extra on top.

Land Banking: This involves buying undeveloped land in an area you believe will grow in value, like the outskirts of a major city, and holding it for several years before selling. It requires patience but can offer substantial returns.

Commercial Properties: Think small shops, office spaces, or warehouses. This can provide higher yields than residential property but often comes with more complex management responsibilities.

The Stock Market Route: Opportunities on the Colombo Stock Exchange

Building on that foundation of long-term asset growth, let’s talk about a completely different animal: the stock market. I think for many people, the Colombo Stock Exchange (CSE) feels a bit intimidating, but its biggest advantage is accessibility. You don’t need millions of rupees to start. You can buy a small piece of a large company with just a few thousand, and unlike property, you can sell your shares in minutes. This liquidity is a huge plus if you ever need cash quickly.

Of course, with great potential comes great risk. The possibility for high returns is very real, but so is the volatility. Just look at 2022. The All Share Price Index (ASPI) hit an all-time high of 13,462.39 in January, only to plummet to around 7,300 by mid-year due to the economic crisis, as noted in the Central Bank’s annual report. That kind of swing can be tough on the nerves and shows why you absolutely must do your own research. You’re not just buying a stock; you’re betting on the company and the broader Sri Lankan economy.

Sectors I’m Watching

So where do you look for opportunities? I tend to focus on a few key areas. Banking and finance stocks are often a good proxy for the overall economy’s health. The tourism and leisure sector is another one; with tourist arrivals surpassing 1.48 million in 2023—the highest since 2019—companies in this space have seen a strong recovery. I also keep an eye on export-oriented manufacturing and the small but growing technology sector. Diversifying across these can help manage some of the risks.

How to Get Started

Getting your foot in the door is surprisingly straightforward. Your first step is opening a Central Depository System (CDS) account through a registered stockbroker. You can choose a traditional firm that offers advice or a low-cost online platform if you prefer to make your own decisions. Once you’re set up, you can start small. Pick a company you understand, read its annual report, and maybe look at a simple metric like its Price-to-Earnings (P/E) ratio to see if it’s reasonably valued compared to its peers. So, are you ready to do a little homework for potentially big rewards?

Head-to-Head: Which Asset Class Suits Your Goals?

Building on that foundation, let’s be honest, theory is one thing, but putting your hard-earned rupees to work is another. I think the best way to figure this out is to put property and stocks side-by-side. It’s a classic matchup, and the winner really depends on your personal circumstances.

Think of it like this:

Capital Required: Property is the high-roller’s game. You need a significant down payment, often millions of rupees, just to get started. Stocks, on the other hand, are incredibly accessible. You can begin with as little as LKR 10,000.

Liquidity: Need your cash back quickly? Stocks win, hands down. You can sell your shares on the Colombo Stock Exchange within days. Selling a house or a piece of land? That can take months, sometimes even years.

Management Effort: Owning property is like a part-time job—finding tenants, handling repairs, chasing rent. It’s active. Stock investing, especially if you follow a “buy and hold” strategy, is far more passive.

Risk & Returns: Property feels tangible and safe, offering rental income and long-term appreciation. But your risk is concentrated in one asset. Stocks are more volatile in the short term, but they offer diversification and potentially higher growth through capital gains and dividends.

The Devil in the Details: Taxes and Currency

Here’s where a little local knowledge goes a long way. When you buy property in Sri Lanka, you’re hit with a stamp duty of around 3-4% right away. The silver lining? Any profit you make when you sell—the capital gain—is currently tax-exempt, which is a massive advantage. For stocks, the game is different. You’ll face a 15% withholding tax on any dividends you receive. It’s a direct cut from your earnings.

And what about our fluctuating rupee? This is a big one. Real estate has traditionally been a fantastic hedge against LKR depreciation. As the currency weakens, property values in rupee terms tend to climb. Stocks can be a hedge too, especially if you invest in export-oriented companies earning in dollars, but their prices are also swayed by overall market sentiment, which can be fickle during economic uncertainty.

Strategic Allocation: Building a Balanced Portfolio for the Future

Alright, let’s talk strategy. I find people often get stuck on an “either/or” debate between property and stocks. But honestly, I think that’s the wrong way to look at it. Your goal isn’t to pick one winner; it’s to build a team of assets that work together. In Sri Lanka, where economic winds can shift quickly, diversification is your best friend. It’s about not putting all your eggs in one basket, so a downturn in one area doesn’t sink your entire ship.

Finding Your Mix

So, how do you actually put this all together? Your personal mix depends entirely on your age, financial goals, and how much risk you’re comfortable with. Here are a few starting points I often discuss with friends:

Conservative (Low Risk): Ideal if you’re nearing retirement. You might put 50% in fixed-income like government bonds or fixed deposits, which were offering around 13% in late 2023 according to the Central Bank. Then, maybe 30% in a stable residential property and just 20% in blue-chip stocks.

Moderate (Balanced): This is for someone with a 10-20 year horizon. Think 40% stocks, 30% real estate, and 30% fixed income. You’re capturing the growth of both markets while keeping a solid safety net.

Aggressive (High Growth): A younger investor could go heavy on stocks—say, 60%—to capitalize on growth like the 30% surge the Colombo Stock Exchange’s ASPI saw in 2023. The rest could be 25% in a high-potential land plot and 15% in fixed income for some stability.

Let’s take a practical example. Imagine Nimali, a 35-year-old professional saving for her child’s university education in 15 years. She could adopt a moderate strategy. She might invest in a small apartment in a Colombo suburb, banking on steady appreciation like the 12.8% gain seen in Colombo’s Land Valuation Indicator in the first half of 2023. Simultaneously, she’d allocate a portion of her monthly savings to a mix of fundamentally strong stocks and keep a buffer in high-interest FDs. This way, she balances the steady, tangible growth of property with the higher potential returns of the stock market.

Ultimately, this is about building a plan that lets you sleep at night. Your allocation isn’t set in stone; review it annually and adjust it as your life changes. The aim is steady, long-term wealth creation, not a get-rich-quick scheme.

So, What’s the Smart Move?

Honestly, I think the biggest takeaway isn’t about picking a “winner” between property and stocks. It’s about understanding yourself. The best investment for you in Sri Lanka truly depends on your own financial story, your goals, and frankly, what helps you sleep at night. Are you aiming for tangible, long-term security with real estate, or the dynamic growth potential that stocks can offer? Neither is universally better; it’s about which one aligns with the future you’re trying to build.

Your most powerful next step isn’t to pick an investment, but to define your destination. Grab a pen and paper and outline your financial goals for the next five years. Once you have that clarity, a certified financial advisor here in Sri Lanka can help you draw the perfect map to get there.

Frequently Asked Questions

Is it a good time to invest in Sri Lanka?

While challenges remain, the post-crisis recovery presents unique opportunities. Lower asset prices and ongoing economic reforms are attracting investors, but thorough research and due diligence are crucial before committing capital.

Can foreigners buy property in Sri Lanka?

Yes, foreigners can buy condominium properties (apartments) from the ground floor up. Land ownership has more restrictions, often requiring a long-term lease or purchase through a majority Sri Lankan-owned company. Seeking legal advice is highly recommended.

What is the minimum amount to invest in the Colombo Stock Exchange?

The minimum investment is very low, often just the price of a single share plus small brokerage fees. You can typically start with as little as LKR 10,000 to 20,000, making it a highly accessible investment option for many Sri Lankans.

Facebook

X

LinkedIn

WhatsApp

Daily News Digest

Get the top stories delivered to your inbox every morning. No spam, ever.

Many Sri Lankan artisans believe that getting their products onto global platforms like Amazon and eBay is a logistical nightmare reserved only for large exporters. You might have a stunning

The most expensive myth for foreign investors is that buying a property in a famous US city guarantees Airbnb success. This assumption is a fast track to disappointment. The truth

Most import ventures from Sri Lanka fail before their first container even docks. It’s not a lack of US demand for Ceylon cinnamon or fiery Jaffna curry powder; it’s a

Have you ever had a truly amazing Sri Lankan meal, maybe a lamprais fresh out of the banana leaf, and thought, “Wow, more people in America need to experience this”?