An inheritance from a relative in Colombo lands in your Sri Lankan bank account. You might see it as a private family matter, but to the IRS, it’s a potentially reportable event. Ignoring this could be a severe misstep, as willful failure to report foreign accounts can trigger penalties up to 50% of the account’s value, a fact reinforced by the IRS’s aggressive enforcement under the Foreign Account Tax Compliance Act (FATCA).

As a U.S. person, your worldwide income is subject to U.S. tax, and your foreign financial assets require disclosure. The complexity, however, lies in the details. You must distinguish between the reporting requirements for the FBAR (FinCEN Form 114) and Form 8938, as they have different filing thresholds and are submitted to separate government agencies—a nuance that trips up many taxpayers.

This article will provide the specific guidance you need. You will learn precisely how to report income from Sri Lankan fixed deposits, manage currency fluctuations for reporting purposes, and correctly determine if your accounts meet the threshold for disclosure. We will provide a clear path to compliance, ensuring your financial ties to Sri Lanka do not become an unforeseen liability.

Who Needs to Report? Your U.S. Tax Obligations Worldwide

Here’s a startling fact: a 2019 survey by Greenback Expat Tax Services found that only 40% of Americans living abroad were aware they needed to file U.S. taxes. This gap in understanding can lead to significant penalties. The foundation of U.S. tax law for individuals rests on a simple but far-reaching principle: if you are a ‘U.S. person,’ your worldwide income is subject to U.S. income tax, regardless of where you live or where that income was earned. That interest accumulating in your Sri Lankan savings account? The IRS wants to know about it.

Defining a ‘U.S. Person’

The term ‘U.S. person’ is broader than many assume. The IRS defines it as anyone who is a:

U.S. Citizen, whether by birth in the United States or through naturalization.

Green Card Holder, officially known as a Lawful Permanent Resident. Your filing obligation doesn’t end if you move outside the U.S.; it continues as long as you hold the green card.

Resident Alien, a non-citizen who meets specific residency criteria for tax purposes, most commonly through the Substantial Presence Test.

The Substantial Presence Test Explained

This is where things get technical, but the logic is straightforward. You are considered a U.S. resident for tax purposes if you meet this two-part test. First, you must be physically present in the U.S. for at least 31 days during the current tax year. Second, your total presence over a three-year period must equal or exceed 183 days, using a weighted formula. The calculation is: all the days you were present in the current year, plus one-third of the days from the year before, plus one-sixth of the days from two years prior.

For example, imagine you were in the U.S. for 120 days in 2024, 60 days in 2023, and 120 days in 2022. Your total would be 160 days (120 + (60/3) + (120/6) = 120 + 20 + 20). In this scenario, you would not meet the 183-day threshold and might avoid being classified as a resident alien for that year, assuming no other factors apply.

From Colombo to Your 1040: How to Report Foreign Income

In 2021, over 1.6 million U.S. taxpayers claimed nearly $28.3 billion in foreign tax credits, according to the IRS. That figure underscores a critical reality for U.S. citizens and resident aliens: the U.S. taxes worldwide income. Let’s shift gears for a moment and break down exactly what that means for your Sri Lankan assets. The IRS expects you to report income from all sources, both foreign and domestic, and it defines “income” quite broadly.

You must report any earnings, even if they never physically enter a U.S. bank account. This isn’t limited to a salary from a job in Colombo. The most common types of reportable foreign income include:

Wages and salaries earned for services performed in Sri Lanka.

Interest income from Sri Lankan savings accounts or fixed deposits.

Dividends received from Sri Lankan companies.

Rental income from a property you own in Galle or Kandy.

Royalties from intellectual property licensed in the region.

From Rupees to Dollars on Your Return

Reporting this income isn’t as simple as adding a line item to your Form 1040. You must first convert all foreign currency amounts into U.S. dollars using a consistent, recognized exchange rate. For example, if your savings account at Sampath Bank earned 150,000 LKR in interest, you would convert that to USD and report it on Schedule B, Part I (Interest), which then flows to your main Form 1040. Similarly, rental income and expenses are tallied on Schedule E.

To prevent double taxation—paying tax to both Sri Lanka and the United States on the same income—the tax code provides two powerful tools. The Foreign Tax Credit (Form 1116) allows you to claim a dollar-for-dollar credit for income taxes you’ve already paid to the Sri Lankan government. Alternatively, the Foreign Earned Income Exclusion (Form 2555) lets you exclude a significant portion of your foreign wages from U.S. taxation, provided you meet strict residency tests. Choosing between these options depends entirely on your specific financial situation.

FBAR vs. Form 8938: Reporting Your Sri Lankan Bank Accounts

Since the Foreign Account Tax Compliance Act (FATCA) was enacted, global tax authorities have exchanged information on an astounding 113 million financial accounts, representing over €11 trillion in assets as of 2022, according to the OECD. This massive data-sharing network means U.S. tax authorities have unprecedented visibility into foreign holdings. And this is where things get practical for anyone with assets in Sri Lanka.

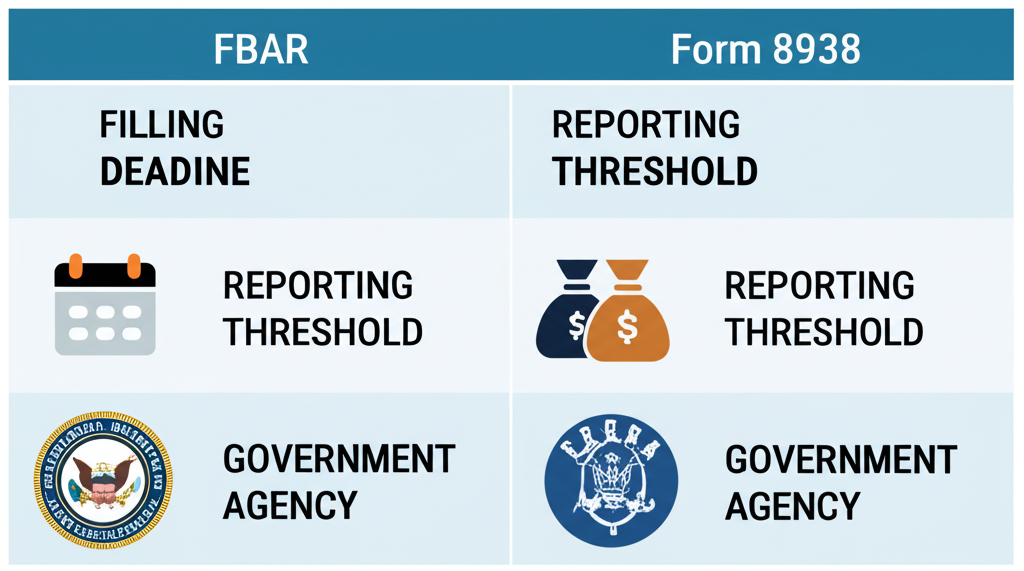

Many people mistakenly believe that filing one foreign account form covers all their obligations. In reality, you might need to file two separate reports with two different government agencies. The requirements are distinct and non-negotiable.

FinCEN Form 114 (FBAR)

The first is the Report of Foreign Bank and Financial Accounts (FBAR), filed electronically as FinCEN Form 114. This is not an IRS form; it goes to the Treasury’s Financial Crimes Enforcement Network (FinCEN). The FBAR is triggered if the aggregate value of all your foreign financial accounts exceeds $10,000 at any point during the calendar year. The threshold is relatively low, and penalties for non-willful violations can reach $14,489 per account, per year.

IRS Form 8938

The second is IRS Form 8938 (Statement of Specified Foreign Financial Assets). This form is part of your annual income tax return. Its reporting thresholds are much higher and depend on your filing status and whether you live in the U.S. or abroad. For a single individual living in the U.S., the threshold is met if you have more than $50,000 in specified foreign assets on the last day of the year or more than $75,000 at any time during the year.

Consider this scenario: You are a single U.S. resident with a savings account at Commercial Bank of Ceylon holding $8,000 and a fixed deposit at Sampath Bank with $7,000. Your total aggregate value is $15,000. This amount requires you to file an FBAR. However, since the total is below the $50,000 threshold for Form 8938, you would not need to file that form, assuming the value never exceeded $75,000 during the year. If that Sampath Bank deposit was $50,000 instead, you would need to file both forms. Filing one does not satisfy the requirement for the other.

The U.S.-Sri Lanka Tax Treaty: Your Shield Against Double Taxation

While over 60% of international tax disputes involve corporate transfer pricing, for individuals, the most common conflicts arise from residency status and pension income, according to 2022 OECD data. The default U.S. rule taxes citizens and residents on worldwide income, creating a direct conflict for anyone with financial ties to Sri Lanka. But wait — there’s more to consider. An international agreement exists specifically to resolve these clashes.

The U.S.-Sri Lanka income tax treaty, signed in 1985 and updated by a 2002 protocol, serves one primary purpose: to prevent the same dollar from being taxed by both Washington D.C. and Colombo. As outlined in Article 23, its main mechanism is the foreign tax credit, which allows a U.S. taxpayer to reduce their U.S. tax bill by the amount of income taxes paid to Sri Lanka. This directly prevents your earnings from being taxed twice.

Key Provisions and the ‘Tie-Breaker’ Rule

The treaty sets clear rules for different income types. It generally grants the recipient’s country of residence the exclusive right to tax pensions and social security payments. For investment income, it caps the withholding tax rate that the source country can apply to dividends and interest, typically at 15%. The most powerful provision for individuals is the residency ‘tie-breaker’ rule. If you are considered a resident of both countries under their domestic laws, the treaty establishes a series of tests—such as the location of your permanent home or your ‘center of vital interests’—to assign residency to just one country for tax purposes.

How to Claim Treaty Benefits

To formally claim that a treaty provision overrides U.S. tax law, you must file Form 8833, Treaty-Based Return Position Disclosure, with your tax return. For example, a U.S. citizen who lives full-time in Kandy and qualifies as a Sri Lankan resident under the treaty’s tie-breaker rule would attach Form 8833 to their Form 1040 to explain why they are excluding certain Sri Lankan business profits from U.S. taxation. You don’t always need to file it, though. Per IRS instructions, the disclosure requirement is waived for claiming treaty-reduced withholding rates on U.S.-source dividends and interest paid to a Sri Lankan resident, a common and practical exception.

Penalties and Pathways: What to Do If You’re Behind on Reporting

Consider this: for a willful failure to file a Foreign Bank and Account Report (FBAR), the IRS can penalize you the greater of $100,000 or 50% of the highest balance in your unreported account for each year of the violation. That is not a misprint. A simple oversight can have financially devastating consequences, showing just how seriously the U.S. government views offshore tax compliance.

The High Cost of Non-Compliance

The penalties extend beyond that single, stark figure. A non-willful FBAR violation can still cost you up to $10,000 per unreported account. Separately, failing to file Form 8938 (Statement of Specified Foreign Financial Assets) triggers an initial $10,000 penalty. If the IRS notifies you and you still do not file, the penalty can grow by another $10,000 for each 30-day period of non-compliance, up to a $60,000 maximum. In the most serious cases, willful non-compliance can lead to criminal prosecution, with potential fines up to $250,000 and five years of imprisonment.

Amnesty and Disclosure Programs

If you have discovered an oversight, there are official pathways for taxpayers to come forward voluntarily. The most common is the Streamlined Filing Compliance Procedures. This program is specifically designed for U.S. taxpayers whose failure to report foreign assets was non-willful. For example, a U.S. citizen living in Sri Lanka who mistakenly believed their local income and bank accounts were not subject to U.S. reporting could potentially qualify. To use this program, you must file amended tax returns, submit all overdue information returns, and certify under penalty of perjury that your past conduct was not intentional.

Getting Compliant

For simpler situations, other options exist. If you do not need to amend your tax returns (meaning you reported and paid tax on all income but simply missed filing the FBAR), you may be able to use the Delinquent FBAR Submission Procedures. Similarly, the Delinquent International Information Return Submission Procedures can be used for forms like the 8938 if you have reasonable cause for the failure and are not under an IRS examination. The correct path depends entirely on your specific circumstances. Navigating these options requires care, which is why consulting a tax professional with cross-border experience is not just a suggestion; it is a necessity.

Your Financial Future: From Colombo to Compliance

Willful failure to report a foreign bank account can result in an IRS penalty of up to 50% of the account’s balance. This staggering figure underscores that compliance is not merely about ticking boxes; it is about safeguarding the very assets you have built in Sri Lanka. The single most effective action you can take is to maintain full transparency with U.S. tax authorities, transforming a complex obligation into a shield for your financial well-being. The U.S. international tax code contains over 7,700 pages of regulations. To ensure your reporting is accurate and your assets are protected, the most prudent next step is to consult a tax professional specializing in expatriate financial matters.

Frequently Asked Questions

Do I have to report interest from my Sri Lankan fixed deposit to the IRS?

Yes. As a U.S. person, you must report your worldwide income, which includes any interest earned from foreign bank accounts, such as a fixed deposit in Sri Lanka. This is typically reported on Schedule B of your Form 1040.

My bank accounts in Sri Lanka never totaled more than $10,000. Do I still need to report them?

If the aggregate value of all your foreign financial accounts did not exceed $10,000 at any point during the calendar year, you are not required to file an FBAR (FinCEN Form 114). However, you may still have a requirement to file Form 8938 if you meet its separate, higher reporting thresholds.

Can I use the Foreign Tax Credit for taxes I paid in Sri Lanka?

Yes, you can generally claim a credit for income taxes paid or accrued to Sri Lanka on your U.S. tax return using Form 1116. This helps prevent double taxation on the same income.

Facebook

X

LinkedIn

WhatsApp

Daily News Digest

Get the top stories delivered to your inbox every morning. No spam, ever.

Many Sri Lankan artisans believe that getting their products onto global platforms like Amazon and eBay is a logistical nightmare reserved only for large exporters. You might have a stunning

The most expensive myth for foreign investors is that buying a property in a famous US city guarantees Airbnb success. This assumption is a fast track to disappointment. The truth

Most import ventures from Sri Lanka fail before their first container even docks. It’s not a lack of US demand for Ceylon cinnamon or fiery Jaffna curry powder; it’s a

Have you ever had a truly amazing Sri Lankan meal, maybe a lamprais fresh out of the banana leaf, and thought, “Wow, more people in America need to experience this”?