You found the perfect apartment, but the landlord wants a six-month security deposit. The reason? You have no US credit history. Your solid financial standing back in Colombo means nothing here.

This frustrating scenario is a common roadblock for newcomers. The American financial system operates on a credit score you don’t have yet, creating a catch-22: you can’t get credit without a history, and you can’t build a history without getting credit. It feels impossible, but there are specific pathways around this problem.

This article breaks that cycle with a practical roadmap. We will walk you through the exact steps to apply for your first secured credit card—often with just a passport and a US bank account. You’ll also learn about credit-builder loans from specific community banks and how to use services like rent reporting to accelerate your progress, building a strong FICO score from zero and unlocking your financial life in America.

The ‘Credit Ghost’: Why Your Sri Lankan History Doesn’t Transfer

You may have been a model borrower in Sri Lanka. Perhaps you paid off a car loan in Colombo without a single late payment and maintained a stellar CRIB report for years. Here is the hard truth: in the United States, none of that history comes with you. When you arrive, you are what’s known as a ‘credit ghost’—to American lenders, you simply don’t exist financially.

The US credit system operates in its own closed ecosystem. Lenders make decisions based on data collected by three national credit bureaus: Experian, Equifax, and TransUnion. These bureaus have no connection to Sri Lanka’s CRIB system. They don’t share data, interpret foreign reports, or translate your past financial discipline. A US bank can’t pull your CRIB report to approve a credit card application; they can only check for a file linked to your Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN).

A Clean Slate Is an Opportunity

Think of it like this. Anura, a software engineer from Kandy, had a premium credit card and a perfect repayment history. After moving to California, he was denied a basic apartment lease without paying a three-month security deposit. The leasing office ran his SSN and found nothing. Anura wasn’t a bad risk; he was an unknown risk. His excellent Sri Lankan history was invisible.

This clean slate, while initially frustrating, is a unique opportunity. You get to build a strong American financial identity from zero, without any past missteps. The entire system is based on a few key factors, with the FICO Score being the most common model used by over 90% of top lenders. Your goal is to start generating positive data points that feed this model. For instance, payment history accounts for 35% of your FICO score, so your immediate focus should be on establishing an account and paying it on time, every time. While most foreign credit doesn’t transfer, some programs like the American Express Global Transfer can help if you were an Amex cardholder in Sri Lanka, offering a rare shortcut to your first US credit card.

Your Foundation: Getting an SSN or ITIN

Speaking of which, your excellent credit history from Sri Lanka unfortunately means very little to US lenders. To them, you’re starting from scratch, and the first piece of the puzzle is a government-issued number. Think of it as your financial passport in the United States—you can’t go far without it.

The Social Security Number (SSN): Your Primary Key

The Social Security Number (SSN) is the nine-digit identifier that nearly every lender, landlord, and utility company will ask for. It’s the gold standard. You can apply for an SSN as soon as you receive authorization to work from the Department of Homeland Security. You’ll simply take your documents, like your passport and work visa, to a local Social Security Administration office. With an SSN, the door to every credit product is open to you.

The ITIN: A Solid Alternative

But what if you aren’t authorized to work yet? You still have a solid path forward. You can apply for an Individual Taxpayer Identification Number (ITIN) from the IRS using Form W-7. While its main purpose is for filing taxes, a growing number of financial institutions accept it in place of an SSN for opening accounts.

Take Rohan, a student on an F-1 visa who can’t get an SSN right away. He applies for an ITIN. Once it arrives in the mail, he walks into a Bank of America branch and uses his ITIN, passport, and a utility bill to open a checking account and a secured credit card. He just took his first official step. A handful of major banks are known to be ITIN-friendly, including:

Bank of America

Capital One

Citi (for certain accounts)

Getting your SSN or ITIN isn’t just a suggestion; it’s the foundational action you must take to begin building your American credit story.

Your First Credit-Building Tools: Top 3 Options

Here’s the part most people miss: you don’t need a pre-existing credit history to start building one. Your responsible financial habits from Sri Lanka unfortunately don’t transfer to the US credit bureaus—Experian, Equifax, and TransUnion. You are starting with a blank slate. The key is to open a US-based account that reports your payment activity to these agencies. These three tools are the most reliable and accessible ways to do just that.

1. The Secured Credit Card: Your Best First Step

A secured card is the single best entry point into the US credit system. It works like this: you provide a refundable security deposit to the bank, typically between $200 and $500. That deposit becomes your credit limit. Because your own money “secures” the line of credit, the bank takes on almost no risk, making it very easy to get approved, often even with just an Individual Taxpayer Identification Number (ITIN) if you don’t have a Social Security Number (SSN) yet.

How to use it effectively: Treat it like a debit card for one small, recurring purchase. For example, use it only for your monthly Netflix subscription or a tank of gas. Then, pay the balance in full before the due date. This demonstrates consistent, on-time payments—the single most important factor (35%) in your FICO Score. After 6-12 months of responsible use, many banks will refund your deposit and upgrade you to a traditional, unsecured card.

2. The Credit-Builder Loan: A Forced Savings Plan

This tool works in reverse from a typical loan. Instead of getting cash upfront, a lender places the loan amount (e.g., $1,000) into a locked savings account. You then make fixed monthly payments over a set term, like 12 or 24 months. Each on-time payment is reported to the credit bureaus. Once you’ve paid the loan in full, the bank releases the funds to you. It’s a disciplined way to build credit while simultaneously saving money. This is an excellent option if you want a “set it and forget it” method that doesn’t tempt you with a spending limit.

3. Becoming an Authorized User: A Relationship-Based Boost

If you have a trusted family member or close friend in the US with a long and positive credit history, ask them to add you as an “authorized user” on one of their oldest credit cards. You don’t even need to use the physical card they send you. Their history with that account—its age, its payment record, its credit limit—can then appear on your credit report. This can give you a significant head start. However, this path comes with a serious warning: if the primary cardholder misses a payment or runs up a high balance, that negative activity will also damage your developing credit file. Only consider this with someone whose financial habits you trust completely.

Smart Habits for a Strong Score: The Rules of the Game

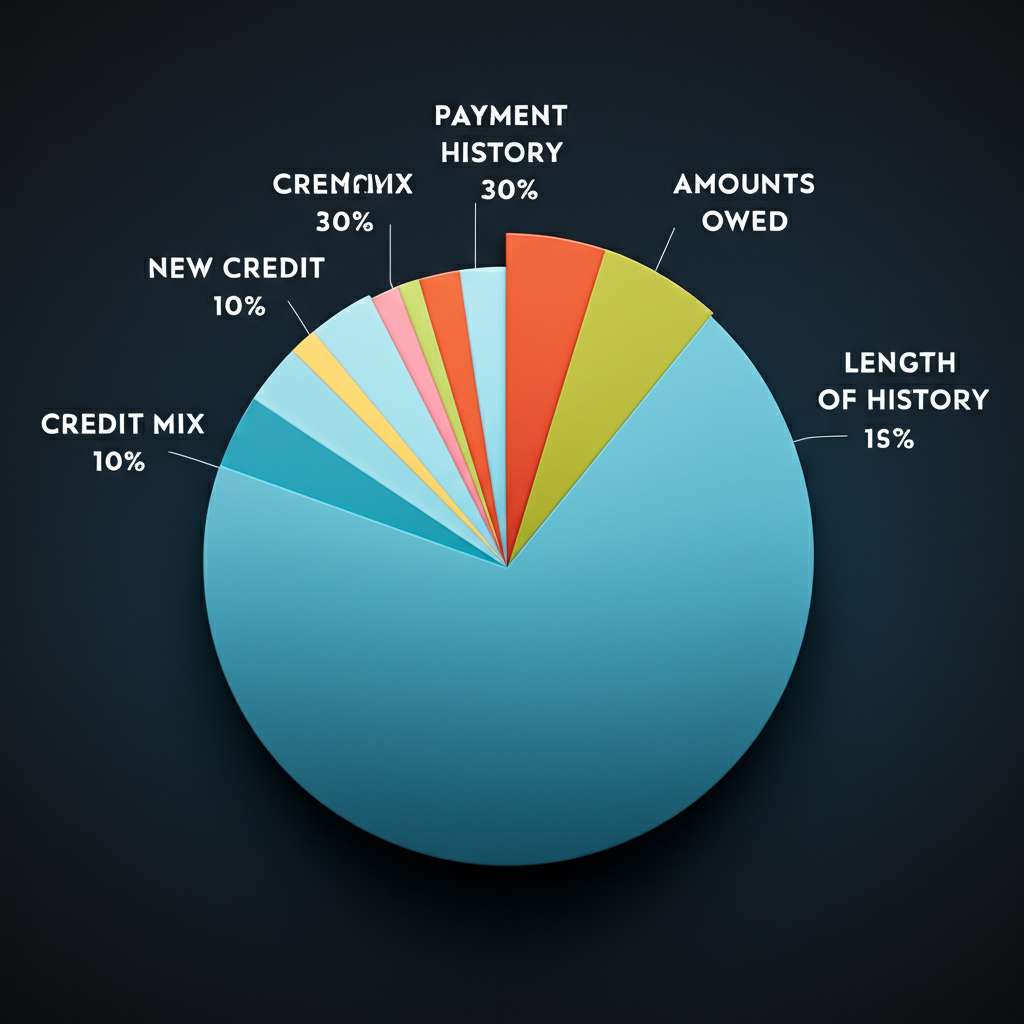

Here’s what really matters though. Once you have that first secured card or loan, you are officially in the game. The US credit system primarily uses a model called the FICO Score, which over 90% of lenders consult to judge your reliability. Think of it as a trust score ranging from 300 to 850. To build a strong one, you just need to follow a few simple rules.

Rule 1: Payment History is King

The single biggest factor in your score—a massive 35%—is your payment history. This means one thing: pay every bill on time, every time. A single payment reported as 30 days late can damage your score for years. The easiest way to guarantee this is to set up automatic payments from your new US bank account for at least the minimum amount due. There are no acceptable excuses for being late.

Rule 2: Master the 30% Rule

Next is what you owe, known as your credit utilization. This makes up 30% of your score. The guideline is to keep your reported balance below 30% of your credit limit. For example, if you get a secured card with a $500 limit, aim to have a statement balance under $150. If you need to spend more, try to pay down the balance before your statement closes. Lenders see low utilization as a sign of excellent financial management, not a lack of spending.

Rule 3: Patience is a Virtue

When you start getting pre-approved offers, it’s tempting to apply for them all. Don’t. Every application can trigger a “hard inquiry,” and too many in a short time signals risk. This “New Credit” category is 10% of your score. Remember, FICO needs at least six months of activity to even generate a score for you. Focus on managing one or two accounts perfectly for the first year. Slow and steady wins this race.

Rule 4: Check Your Work

You can’t improve what you don’t measure. US law gives you the right to a free credit report from each of the three major bureaus (Equifax, Experian, and TransUnion) every year. The only official government-mandated site for this is AnnualCreditReport.com. Pull your reports, check them for accuracy, and confirm that your good habits are being recorded correctly. Think of it as a regular check-up for your financial health.

Common Pitfalls: Mistakes That Can Set You Back Years

As a newcomer from Sri Lanka, you arrive with a blank slate. Your responsible financial history back home doesn’t transfer to US credit bureaus like Experian, Equifax, or TransUnion. This fresh start is an opportunity, but it also means your new credit profile is fragile. A few early mistakes can cause damage that takes years to repair. Think of it this way: your first few financial actions carry immense weight.

The Lure of “Easy Money” and High Balances

When you need cash quickly, high-interest payday loans or cash advances can seem like a lifeline. They are not. These products are financial traps designed to keep you in a cycle of debt with astronomical fees. Avoid them completely. A more subtle mistake involves your first credit card. Let’s say you get a secured card with a $500 limit. You put a $450 purchase on it, intending to pay the bill in full. While you avoided interest, your credit report for that month shows a 90% credit utilization ratio. Lenders see this as a sign of risk. This single action heavily impacts the “Amounts Owed” category, which makes up 30% of your FICO score. Always aim to keep your balance below 30% of your total credit limit—even if you pay it off every month.

Mistakes of Trust and Neglect

You may be asked to co-sign a loan or credit card for a friend or family member who can’t get approved on their own. Be extremely cautious. When you co-sign, you are legally promising to pay the entire debt if the primary borrower cannot. Their missed payments will appear on your credit report, directly damaging your score. Finally, don’t assume your credit report is accurate. Identity mix-ups and clerical errors are common. You must be your own advocate. Check your free credit reports annually from all three bureaus. A single uncorrected error, like a late payment that wasn’t yours, can prevent you from getting an apartment or a car loan when you need it most.

Your American Financial Story Begins Now

Building your US credit history isn’t about complex financial maneuvers; it’s about one consistent habit. Consider a newcomer from Colombo who gets a secured credit card. He uses it only for his monthly phone bill—a predictable expense—and sets up automatic payments to clear the balance in full. This single, disciplined action, repeated month after month, is the most powerful signal you can send to lenders. It proves your reliability and builds a strong foundation faster than any other method.

This isn’t a distant goal; it’s a task for today. Your immediate next step is to research secured credit cards offered by major banks. Compare their requirements, choose one that fits, and submit your application. Taking this concrete step moves you from planning to actively building the credit score that will unlock future opportunities, from renting an apartment to financing a car.

Frequently Asked Questions

Can I use my Sri Lankan bank records to get a US credit card?

Generally, no. US lenders primarily use US credit reports from Equifax, Experian, and TransUnion. However, some international banks like American Express may consider your existing global relationship for specific cards under their Global Card Transfer programs.

How long does it take to build a good credit score in the US?

You can establish a FICO score in as little as 6 months with at least one active credit account. Reaching a 'good' score (670+) typically takes 1-2 years of consistent, positive credit habits like on-time payments and low utilization.

What is a good starter credit limit for a newcomer?

For a secured credit card, your limit is usually equal to your security deposit, which is typically between $200 and $500. This is more than enough to start building a positive payment history that will be reported to the credit bureaus.

Facebook

X

LinkedIn

WhatsApp

Daily News Digest

Get the top stories delivered to your inbox every morning. No spam, ever.

Many Sri Lankan artisans believe that getting their products onto global platforms like Amazon and eBay is a logistical nightmare reserved only for large exporters. You might have a stunning

The most expensive myth for foreign investors is that buying a property in a famous US city guarantees Airbnb success. This assumption is a fast track to disappointment. The truth

Most import ventures from Sri Lanka fail before their first container even docks. It’s not a lack of US demand for Ceylon cinnamon or fiery Jaffna curry powder; it’s a

Have you ever had a truly amazing Sri Lankan meal, maybe a lamprais fresh out of the banana leaf, and thought, “Wow, more people in America need to experience this”?